BELEGA Whitepaper

BLGA.v0.5.OCT.30.2020

Introduction

BELEGA is a start-up that plans to deliver a state

of the art technology platform which allows Small-

Medium Businesses (SME’s) access to the peer-to-peer fundraising market.

The BELEGA platform will allow those SMES

looking to raise funds access to cross-border

Crowdfunding opportunities, and the ability to

build relationships all while working with the

startup community. The aim is to become a

leading global crowdfunding platform for these

SME businesses.

This white paper will explain, in detail, our

strategy and approach to business execution, and

ultimately how we intend to build and delivery a

successful business. All the information contained

within this white paper are subject to the

disclaimers contained at the end of this

document. You should read these before you

continue.

BELEGA will deploy a unique blend of leveraging

its FinTech business experience and a global

network of both startups and investor

relationships. In doing this, BELEGA can offer

SME companies a new, alternative financing opportunity.

BELEGA believes that the crowdfunding market offers SME within underserved areas of the globe, access to

new finance. A great example of this is the African FinTech space It is frequently looking for both European

and Asian seed and growth funding..

BELEGA is confident that it can manage market segments such as this, better than this market better than

other players in the crowdfunding space. This assessment is based on the quality of the team’s background

along with its network.

The business model BELEGA will deploy, intends to enable the company to generate a commission on each

client based on the total amount of funds raised for every project.

The team will be based in Europe and led by FinTech professionals with decades of experience in

developing markets. BELEGA will position itself directly to have access from experts with experience working

with large global technology and finance organisations.

Background

BELEGA was originally based in Malta. Over the last eighteen months, the team has spent a large amount of

time and money with the aim of being regulated by the Malta Financial Services Authority (MFSA). After the

introduction of the Virtual Financial Assets (‘VFA’) Act in 2018, this seemed like a logical step. Using the

benefits of this Act to conduct a legal and regulated Token Sale. During 2018, Malta’s then-Prime Minister

Joseph Muscat presented Malta as a “blockchain island” at the United Nations General Assembly. However,

by the end of 2019, it became apparent to BELEGA that Malta would not follow through on this promise as

no licenses had been issued by the MFSA. As a result, the majority of blockchain, DLT and cryptocurrency

based businesses who moved to Malta, have since left. Including large named such as Binance, the largest

cryptocurrency exchange in the world.

Because of the change in market and failings of the Maltese license issuers, BELEGA made the strategic

decision to change approach entirely. The BELEGA team took the critical decision to exit Malta, and focus

on moving to a jurisdiction which would allow it to meet its fundraising objectives.

BELEGA saw this as an opportunity. An opportunity to re-energise the company and initiate a strategic

revision, allowing us to adapt both the jurisdiction where the raise would be conducted and make the

necessary changes to the business model for planned success. As a result, we entered 2020 with the new

BELEGA.

The BELEGA project has the advantage of nearly three years of project preparation, having passed through

the fluctuation of blockchain interest from sector professionals, amateurs and the mass market. We have

worked closely in Europe and Asia with technology innovators, product design and marketing professionals.

Alongside this, we are now working with top level legal and regulatory professionals and developed

relationships with potential partners who are fundamental to delivering results. Today we use this foundation

to guide our strategy and belief that in 2020 we have developed a strategy, model and business plan to

deliver value.

The Offering

BELEGA is issuing its BLGA token as an Initial Token Offering to generate seed funding, enabling BELEGA

to grow and meet its end goal creating a UK Crowdfunding business. The BLGA Token will fuel the

crowdfunding ecosystem as it may be used by its holder in exchange for BELEGA services at discounted

rates, and will provide participants exclusive project membership benefits.

The project has established relationships with product and user experience experts, licensed technology

partners, licensed payments processors, licensed in the UK and Europe. Leadership is on board and has

been working with the founders to develop the strategy and business model for the past two years. Our short

and long term vision are in place and we have worked through the financial planning exercise to understand

the path to value creation. The next step is to raise the seed funding necessary to initiate the business build.

The Opprtinity

Crowdfunding has brought fintech closer to its customers, as the industry experiences a daily buzz related to

Unicorns, digital banking, a surge in lending, and success stories from crowdfunding capital raises.

After 2008, trust in banks and financial institutions was at an all time low. The global financial collapse sent

the world into a depression, not only financially, but psychologically. The recovery led to a new breed of

financial service provider driven by the alternatives born of the collapse of trust in the regular providers.

Banks, once considered the cornerstones of global finance, failed, and people in growing numbers actively

searched for alternatives.

Fintech has grown as a sector, and although initially in total opposition to the banks, today the relationship

has led to collaboration, partnerships and increasingly, M&A combinations. In FinTech, the focus is on how to

monetise, and the industry has spent a lot of time on this, developing innovative business models,

transactional revenue understanding, and scale.

In our view, the industry is moving in the right direction, but we'd like to approach fintech from another angle,

one where value is created for the companies, and investors. Crowdfunding solutions are providing fastmoving

companies access to capital from a diversified source, eager to be involved based on the press

pouring daily out of the industry. It is common that advanced rounds of funding are being followed by large

crowdfunding rounds and in the meantime, adding to its base of users, as these startup investors, their

friends and family, are the early adopters pushing the product deeper into the market.

In the crowdfunding model, investors evolve into users with influence, and in return, the companies leverage

those investors as sources of feedback, valuable information, and from which to pull ideas for the future

product roadmap. The model enhances communication by providing a direct channel for dialogue to a vested

customer base, creating an environment for developing better products, ultimately driving growth, and ideally,

revenues. This change is taking place across many industries, not just finance. Businesses have learned that

a product-first approach, while forging strong customer relationships through new business models and

investment channels, is creating a modern dynamic with their market for their brand: owners, customers,

companies, and success... democratised.

To set the scene for you, let’s look at the Revolut example. In 2016, a little known pre-paid debit card startup

that allows users to exchange currencies and transfer money internationally with the interbank rate, rather

than the extra fees that banks slap on users, based out of the UK, asked people to contribute into the fintech

startup on crowdfunding platform Crowdcube, and those who did, saw their initial contribution increase in

value by around 19 times initial contribution by August 2018. . As of today, that number is closer to 27 times

initial contribution. . Translated, this means early contributors realised a 2,700 percent return on their original

contribution to the company in just two years. At the moment, contributors have been offered the choice to

either sell their shares back to Revolut or retain them. Today, Revolut is valued at over $1.7B, most recently

launching in Singapore, Japan, and the USA.

Introduction to crowd funding models

- 1. Donation Based Crowdfunding

- The typical example of this type of crowdfunding is the fundraising for humanitarian purposes. People donate their money for a cause, an idea or simply in order to help the organisation making the campaign. In fact, the people who donate don’t expect any type of reward from their actions, they simply hope that the amount they have invested can really help make a difference.

- 2. Rewards Based Crowdfunding

- We can consider the Rewards Based Crowdfunding as the “upgrade” to donation crowdfunding. In fact, very early stage companies make these kind of crowdfunding campaigns in order to finance the production of their future product. By financing the project, the investor will get the product or a discount when the product will be ready for the market. In order to make people invest more money, there are different discount levels that are offered, usually increasing with the amount invested. However, the perception of this kind of crowdfunding is similar to the donation type because you don’t even know if the campaign will reach the target and the production will effectively start. One of the most famous platforms for rewards-based crowdfunding is Indiegogo, in which you can find innovative and hightech products that are going to be produced with the funds of their campaigns.

- 3. Debt Based Crowdfunding

- Think of a bond. A state offers these types of financial instruments in exchange for liquidity. Of course there will be an interest rate that defines the earnings that the investor will get at the end of a fixed period. It works similarly for debt based Crowdfunding. In fact, these campaigns are particularly popular among entrepreneurs who don’t want to give up equity in their start-up companies immediately and/or do not have access to more traditional types of loan facilities. These are also growing in popularity as a way for real estate developer to fund a particular real estate project or projects.

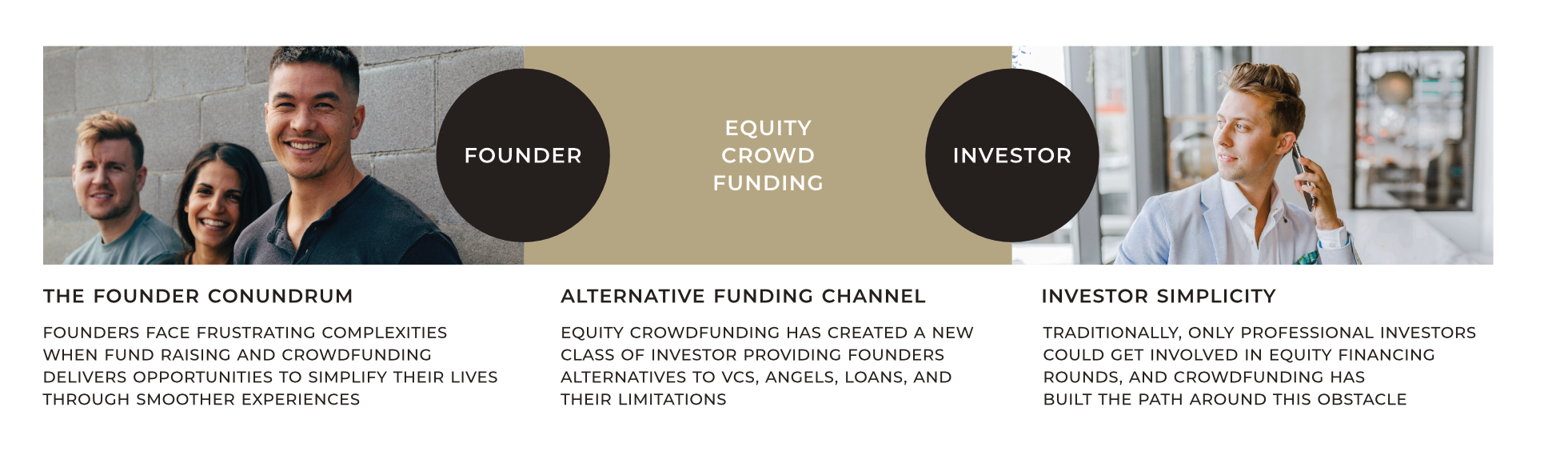

- 4. Equity Based Crowdfunding

- In an equity-based crowdfunding campaign, a person contributing money can expect to receive some ownership of the company that is raising the funds. From another perspective, the company which is running the campaign is selling off a piece of its ownership (e.g., shares, membership interest, etc.) to each of the crowd members who contributed with money. Usually the crowd is interested in participating in this kind of crowdfunding because the equity, that they are buying can address them dividend or can be sold in the future at a higher value. Equity based crowdfunding campaigns are being used more and more by entrepreneurs and start-ups seeking an alternative to traditional venture capital and angel investors when looking for a capital infusion to take their business to the next level.

- 5. [NEW] The Introduction of Blockchain Equity Crowdfunding

- Equity crowdfunding is the most interesting type of crowdfunding for investors who are seeking for great profits. In the the blockchain based equity crowdfunding model, the equities are recorded on a blockchain in order to make use of the advantages that blockchain technology brings. It is immutable too hacks such as DDoSS attacks, which is a problem that even big companies like VISA and Playstation still struggle with. It also allows for a more liquid tradeoff which makes it more accessible. By combining the blockchain technology and the equity crowdfunding, each project will have more visibility and engagement from the investor side, because they are interested in the growing of the company.

Clearly equity crowdfunding is experiencing rapid growth, here are some recent examples:

- 1. Zazu, a Lusaka-based fintech company, announced that it had raised USD 1.4M in funding in its second crowdfunding campaign, it has already announced a third coming soon.

- 2. The UK FinTech Curve, an Over-The-Top banking platform that consolidates multiple cards and accounts into one smart card and app to simplify and unify how people spend, send see and save their money, announced it's first crowdfunding campaign (Crowdcube). Curve offered eligible customers a chance to invest in "one of Europe’s hottest fintech start-ups", enabling them to invest from as little as £10 to own part of the business and gain access to some exclusive shareholder rewards. Curve raised £6m in a fast-paced crowdfunding campaign that saw £4m raised in just 42 minutes. The first £1M took five minutes and the total number of participants ended at just over 9,500 people.

- 3.Arival Bank recently raised $2.3M in a pre-Series A, equity crowdfunding campaign. The Singapore-based FinTech bank for businesses and entrepreneurs soared past its fundraising target of $864,500, and now boasts a pre-money valuation of more than $14.8 million. The campaign marks the first time a digital bank has conducted an equity crowdfunding raise in the USA. Seedinvest, an SEC-licensed broker-dealer platform based in New York, spearheaded the fundraising with Crowdcube in the role of joint partner.

In 2020, many SME’s are looking for new ways to obtain financing for their startup. The world has been

rocked by COVID, and large nations such as the United States have re-entered recession. As a result,

financial institutions are once again, pulling the rug from under many new companies looking to make their

mark.

It is because of this reluctance by traditional financial institutions, that the peer to peer market is moving

forward at a speed the market has not seen in other comparable segments. In recent years, lending and

investing on a peer to peer model, has spread globally as user experiences and business models are reimagined.

Much of what is to come in the next few years will certainly be about consolidation, at all times

enhanced user experience and crucially important, marketing innovation.

The battle for attention is waging and an ethical, yet aggressive solution is what may differentiate a brand.

Let's not forget, the same banks are pouring hundreds of millions into FinTech M&A, into the very same

challengers who spoke so poorly of them publicly in their initial days.

For those watching the industry closely, we know that today's founder/CEO is frustrated by venture capital,

who many say do very little real venture investing, but instead focus on the lowest possible risk investments

working in tandem with their partners as “followers”. Twinning this with the fact that most VC firms are simply

looking for their ‘pound of flesh’ and give little to no care about the company itself. Rather, they place their

focus on the profits to be made and their exit strategy.

Founders and innovators, are looking at alternatives and crowdfunding has become a proven channel for

these different funding rounds. A good performing peer to peer fundraising can expect to reach numbers as

high as $15M, although regulatory hurdles keep these rounds to lower amounts for smaller organisations

(typically less than ~$8M).

This market is driven by great user experiences, promoting ease-of-use for the companies and investors who

expect easy-to-use mobile experiences, and providing holistic, integrated digital lending capabilities, helping

to address the market's changing preferences.

One advantage of the past ~10 years is that the industry is making strides to overcome the fear of mobile,

with user uptake of mobile financial services soaring in global markets, including in the USA where, for

example, Bank of America's digital channel now accounts for 26% of total sales, with mobile representing

over half of these digital sales. And as another good sign for the lending sector, despite this growth, BOAs

strategy to increase these numbers is centered around focused energy on even more advanced areas of

digital account opening, like lending.

In an example of traditional cornerstone investors moving to an online and mobile financial services focus,

Goldman Sachs CEO, David Solomon, recently said, “I think we’re in the early stages of building a digital

platform for consumers that gives them more information, more tools are their disposal. Over the last three

years we’ve built a digital bank with $55 billion in digital deposits, with $5 billion of loans; 4 to 5 million

customers; a brand-new credit card platform and have launched a card with Apple. I feel like that’s pretty

good progress over a short period of time.”

Traditionally, only professional investors could get involved in equity financing rounds, and it's clearly

crowdfunding which has forged the path around this obstacle. In its simplest form, Crowdfunding connects

startups with people in the market who have funds and believe in the plans of these businesses, and this

simple model is expected to grow the industry to over USD 300 billion by 2025.

In the past, traditional investing could lead to a long, tiring, and often rewardless exercise. We believe

crowdfunding innovation can change this, giving companies the chance to engage with investors when their

ideas might otherwise never have come across the desk of a traditional investor. It also allows founders and

their teams to validate their ideas before entering the market, while providing the advantage of converting

investors to loyal customers and brand ambassadors by offering them incentives for their early show of

support.

Equity crowdfunding is creating a new class of investor. There are genuine risks that many people who

become involved do not have adequate investor experience to understand all of the implications of their

investments, or, as a risk to the companies themselves, to be a positive influence on the future of the

business. This places a new responsibility on those backing projects through crowdfunding platforms to

educate themselves, through crowdsourced Due Diligence and progressive community conversation.

Coupled with this level of necessary self-governing responsibility, crowdfunding has the real potential to

become a reliable tool for venture capitalists to achieve a lasting ROI long into the future of fintech.

It is our objective at BELEGA to provide access to capital for developing market SMEs, and access to global

investments for investors who want access to wider portfolio differentiation opportunities. The companies are

being built today, we believe we can accelerate their growth, building our own sustainable crowdfunding

business in the process.

Competition

The team has researched the market and knows our competition well. On the surface, it may appear that

BELEGA is entering a crowded space, but a deeper review of our strategy reveals that the niche market of

developing country startups that we plan to address, is very underserved.

For example, crowdfunding has been steadily gaining traction in Africa over the past decade. Still,

crowdfunding in Africa remains limited compared to other regions: In 2015, the African crowdfunding market

amounted to ~ $70M, accounting for less than 1% of the global crowdfunding market. However, a 2013

World Bank report estimated that by 2025, crowdfunding will be a $96B industry growing at a rate of 300%

per year.

While much has been made of crowdfunding’s potential to transform small business and entrepreneurship

across Africa, there are important challenges and regulatory barriers that we have identified and will address.

One is example is that African entrepreneurs who use crowdfunding platforms are often operating in an

unregulated market. BELEGA will address this by requiring startup companies to make substantial

disclosures when providing Due Diligence information in order for BELEGA to be able to make informed

decisions, and strengthen investor protections.

There are other European based platforms that allow developing country entrepreneurs to pitch their

businesses and raise capital from funders abroad. However, many international platforms simply re-use their

European policies and procedures and fail to address the developing market requirements. We believe our

expertise in this area will differentiate BELEGA and lead to a larger portfolio of startups and investors.

Competition Landscape

Key competition in the crowdfunding sector

Token Economics

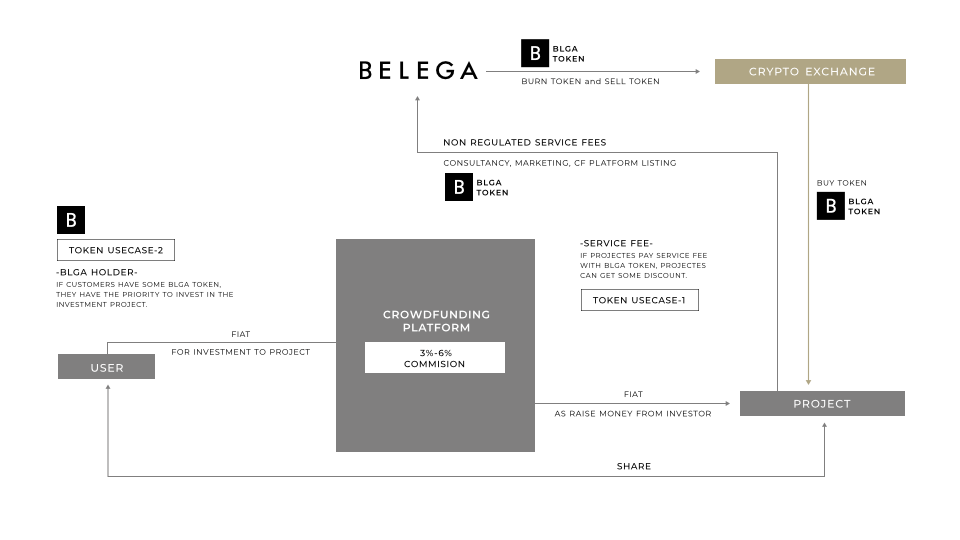

BELEGA tokens are called BLGA. BLGA is a token developed based on ERC-20. This token will be used on

the UK crowdfunding platform as follows: BLGA is a crowdfunding platform feature that supports both

projects and users.

1. As payment of service fee from the project - The project pays for the service for listing on the

crowdfunding platform. The project can receive a substantial discount by paying this payment with BLGA

tokens. Especially for cross-border projects, the project can benefit compared to existing payment methods.

2. Priority to user - If the users of the crowdfunding platform are BLGA holders, they will have the priority to

invest in the projects listed on the platform. For example, when an attractive project is posted on a

crowdfunding platform, BLGA holder users have the priority to invest a few days ahead of users who do not

have a BLGA holder.

3. Future - Adoption of BLGA at partner companies

BLGA Token Offering

BELEGA is issuing its BLGA token as an Initial Token Offering with the aim of raising funds to allow the

company to meet its objectives.

After the raise, the BLGA Token will fuel the crowdfunding ecosystem as it may be used by its holder in

exchange for BELEGA Services at discounted rates, and will provide participants exclusive project

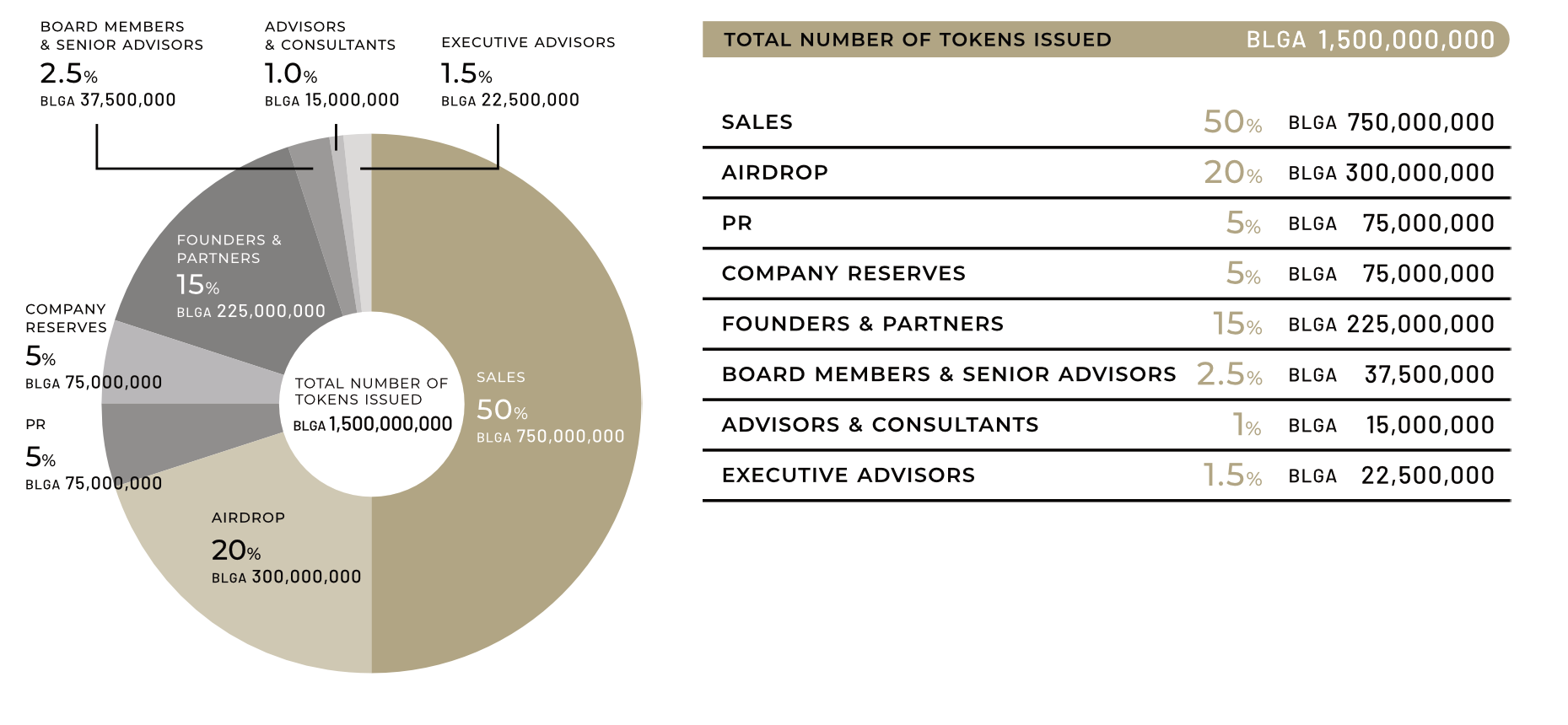

membership benefits.The complete token distribution plan is detailed below:

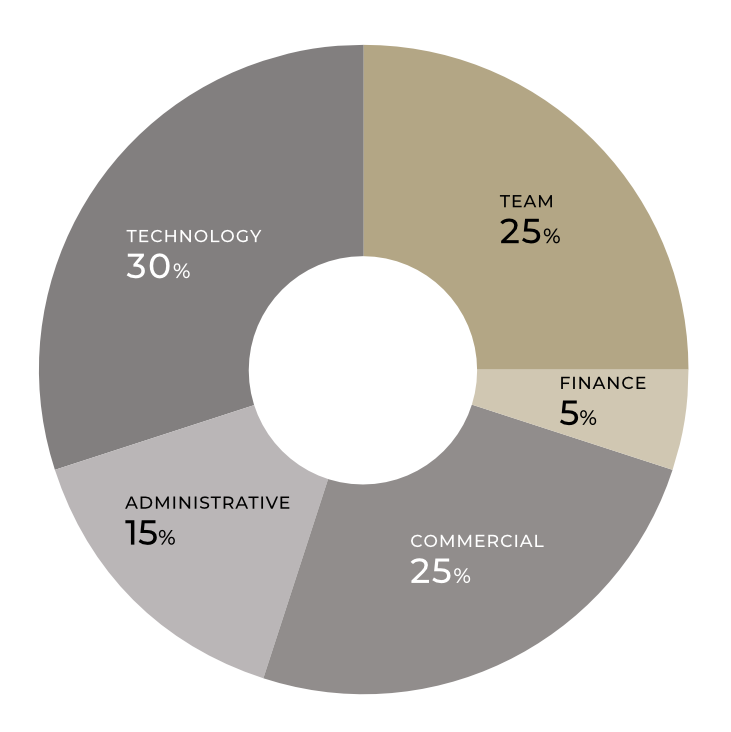

Use of Funds

Following the BLGA Token ICO, the funds are planned to

be deployed to build an SME crowdfunding solution and

execute a go-to-market plan. The funds would enable

BELEGA to launch services catering to underserved

SME founders and alternative investors, in order to

become a strong provider of working capital to SMEs.

This ICO is an opportunity to participate in an

organisation focused on a global FinTech business

model. Funds are planned to cover the costs associated

with developing an FCA regulated company, along with

all the technology requirements to make it operate. The

model to the right is a conceptual use of funds model

that graphically represents how use of funds could be

modeled.

Leadership

To bring the business to life, BELEGA will recruit a FinTech team to build and manage the company from

early stage seed funding, through to full execution of the crowdfunding model.

Executive Management Team

Upon completion of the ICO, funds are intended to be used to recruit key skills required to execute a

European crowdfunding business. Profiles include executive management, finance, product, commercial and

technical, with an emphasis on background that includes bank-grade security and data management.

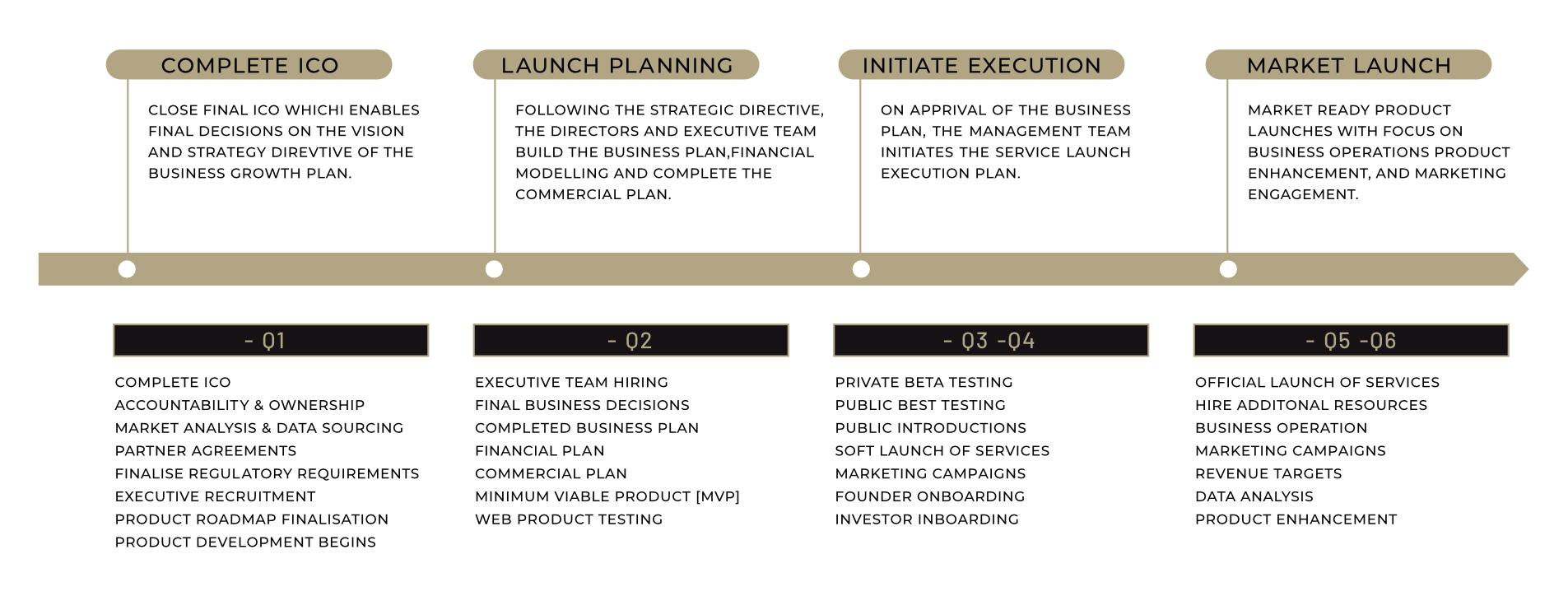

Project Roadmap

What follows is an example of a potential implementation timeline to be developed following the ICO once

leadership and the management is engaged. This is an example of a working plan profile that BELEGA

intends to for the first 12–18 months of operations.

Disclaimer

The information set forth below may not be exhaustive and does not imply any elements of a contractual relationship. While we make every effort to ensure that any material in this white paper is accurate and up to date, such material in no way constitutes the provision of professional advice. Belega does not guarantee, and accepts no legal liability whatsoever arising from or connected to, the accuracy, reliability, currency, or completeness of any material contained in this white paper. Investors and potential Belega token holders should seek appropriate independent professional advice prior to relying on, or entering into any commitment or transaction based on, material published in this white paper, which material is purely published for reference purposes alone.

Belega tokens will not be intended to constitute securities in any jurisdiction. This white paper does not constitute a prospectus or offer document of any sort and is not intended to constitute an offer of securities or a solicitation for investment in securities in any jurisdiction. Belega does not provide any opinion on any advice to purchase, sell, or otherwise transact with Belega tokens and the fact of presentation of this white paper shall not form the basis of, or be relied upon in connection with, any contract or investment decision. No person is bound to enter into any contract or binding legal commitment in relation to the sale and purchase of Belega tokens, and no cryptocurrency or other form of payment is to be accepted on the basis of this WhitePaper. No person is bound to enter into any contract or binding legal commitment in relation to the sale and purchase of Belega tokens, and no cryptocurrency or other form of payment is to be accepted on the basis of this WhitePaper.

This Belega White Paper is for information purposes only. We do not guarantee the accuracy of or the conclusions reached in this white paper, and this white paper is provided “as is”. This white paper does not make and expressly disclaims all representations and warranties, express, implied, statutory or otherwise, whatsoever, including, but not limited to: (i) warranties of merchantability, fitness for a particular purpose, suitability, usage, title or non-infringement; (ii) that the contents of this white paper are free from error; and (iii) that such contents will not infringe third-party rights. and its affiliates shall have no liability for damages of any kind arising out of the use, reference to, or reliance on this white paper or any of the content contained herein, even if advised of the possibility of such damages. In no event will team Belega or its affiliates be liable to any person or entity for any damages, losses, liabilities, costs or expenses of any kind, whether direct or indirect, consequential, compensatory, incidental, actual, exemplary, punitive or special for the use of, reference to, or reliance on this white paper or any of the content contained herein, including, without limitation, any loss of business, revenues, profits, data, use, goodwill or other intangible losses. Belega makes no representations or warranties (whether express or implied), and disclaims all liability arising from any information stated in the white paper. In particular, the “Roadmap” as set out in the text of the white paper is subject to change, which means that Belega is not bound by any representations to the future performance and the returns of Belega. The actual results and the performance of Belega may differ materially from those set out in the Belega White Paper.

lease note that contents of Belega white paper may be altered or updated at any time in future by the project’s management team. The Whitepaper has been prepared solely in respect of Initial Coin Offering of Belega tokens. No shares or other securities of the Company are being offered in any jurisdiction pursuant to the Whitepaper. The Whitepaper does not constitute an offer or invitation to any person to subscribe for or purchase shares, rights or any other securities in the Company. The shares of the Company are not being presently offered to be, registered under Securities Act of any country, or under any securities laws of any state. the tokens referred to in this whitepaper have not been registered, approved, or disapproved by the us securities and exchange commission, any state securities commission in the united states or any other regulatory authority nor any of the foregoing authorities examined or approved the characteristics or the economic realities of this token sale or the accuracy or the adequacy of the information contained in this white paper under, the US. Securities act of 1933 as amended, or under the securities laws of any state of the united states of America or 28 any other jurisdiction. purchasers of the tokens referred to in this whitepaper should be aware that they bear any risks involved in acquisition of Belega tokens, if any, for an indefinite period of time. Some of the statements in the whitepaper include forward-looking statements which reflect Team Belega’s current views with respect to product development, execution roadmap, financial performance, business strategy and future plans, both with respect to the company and the sectors and industries in which the company operates. statements which include the words ''expects'', ''intends'', ''plans'', ''believes'', ''projects'', ''anticipates'', ''will'', ''targets'', ''aims'', ''may'', ''would'', ''could'', ''continue'' and similar statements are of a future or forward-looking nature. all forward-looking statements address matters that involve risks and uncertainties. Accordingly, there are or will be important factors that could cause the group's actual results to differ materially from those indicated in these statements. these factors include but are not limited to those described in the part of the whitepaper entitled '' risk factors '', which should be read in conjunction with the other cautionary statements that are included in the whitepaper. any forward-looking statements in the whitepaper reflect the group's current views with respect to future events and are subject to these and other risks, uncertainties and assumptions relating to the group's operations, results of operations and growth strategy. these forward-looking statements speak only as of the date of the whitepaper. subject to industry acceptable disclosure and transparency rules and common practices, the company undertakes no obligation publicly to update or review any forward-looking statement, whether as a result of new information, future developments or otherwise. all subsequent written and oral forward-looking statements attributable to the Project Belega or individuals acting on behalf of Belega are expressly qualified in their entirety by this paragraph. No statement in the whitepaper is intended as a profit forecast and no statement in the whitepaper should be interpreted to mean that the earnings of Project Belega for the current or future years would be as may be implied in this whitepaper. By agreeing to acquire Belega token I hereby acknowledge that I have read and understand the notices and disclaimers set out above

No regulatory authority has examined or approved of any of the information set out in this white paper. Thus, no action has been or will be taken under the laws, regulatory requirements or rules of any jurisdiction. the publication, distribution or dissemination of this white paper does not imply that the applicable laws, regulatory requirements or rules have been complied with. Please refer to our website for terms & conditions of participating in Belega initial coin offering.